Company Annual Return Filing: All you need to know

Legal & Compliance

344 week ago — 6 min read

Summary: All companies are required to file annual returns with the Ministry of Corporate Affairs (MCA) every year. Here is all you need to know about company annual return filing.

The Companies Act, 2013 lays down provisions containing certain rules and regulations which a ‘company’ whether public or private limited has to abide by, right from the initial stage of ‘incorporation’ to the final stage of ‘dissolution’. This has been done in order to encourage transparency and high standards of corporate governance. All companies (private limited company, one person company, limited company, section 8 company, etc) are required to file an annual return with the MCA every year. In addition to filing MCA annual return, companies would also be required to file income tax return.

Note: Directors of companies that have failed to file the annual return for three years will be disqualified for 5 years.

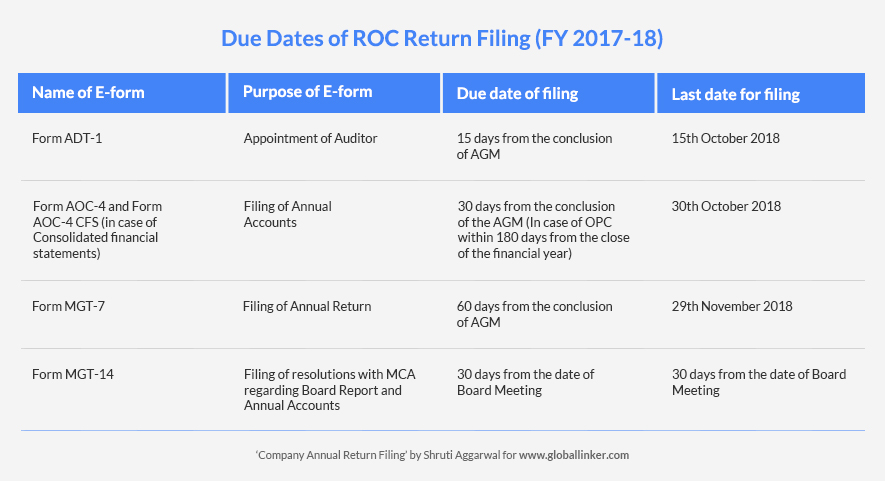

Section 92 and Section 137 of the Act mentions the mandatory filing of the annual return and financial statement of the company before the ROC (Registrar of Companies) within a stipulated time as has been prescribed under the Act.

Provisions relating to the annual filings made to ROC under the Act

Section 92

This section talks about the filing of the annual return to ROC. According to this, it ismandatory for every company to file a copy of the annual return within 60 days from the date on which Annual General Meeting (AGM) or 60 days within the date on which the AGM was scheduled to be held or should have been held in cases where the company failed to conduct an AGM along with the statement specifying the reason for the same accompanied with the fine imposed under Section 403 of the Act. (Ministry of Corporate Affairs, 2013)

(1) The ‘annual return’ of the company must contain information in the Form MGT-7 (e- form) as has been prescribed under the Act. This information includes following as they are at the close of the financial year such as:

1. The registered office of the company, information about its holding, subsidiary and associate companies and principal business activities

2. The pattern of its shareholding and shares, debentures and other securities

3. The indebtedness of the company

4. Members and debenture-holders of the company accompanied with changes made from the close of the previous financial year

5. Promoters, directors, key managerial personnel of the company accompanied with changes made from the close of the previous financial year

6. Meetings of the members, Board and its different committees accompanied with their attendance details

7. Remuneration of directors of the company and its key managerial personnel

8. Penalty or punishment imposed on the company, its directors or officers of the company and details of compounding i.e. settlement of offences and the appeals made against such penalty or punishment

9. Information regarding shares held by or on behalf of the foreign investors along with their names, addresses, countries of incorporation, registration and percentage of shares held by them

10. Such other matters related to the company as may be mentioned and must be signed by a director and the company secretary, or by a company secretary in practice

(2) In case when the annual return is filed by a listed company or, by a company having paid-up capital and turnover as may be allowed under the Act, that company shall obtain certification by a company secretary who is currently practicing, in the mentioned form under the Act, declaring that the annual return mentions the facts correctly and ensure that the company has followed all the provisions of this Act.

Section 137

It deals with the filing of the financial statement by the company. According to this, a copy of financial statement which may include consolidated financial statement approved and adopted at AGM of the company, with all the other documents required to be attached with such statement, must be filed before the office of ROC within 30 (thirty) days of date of the AGM held by the company. This filing must be done through Form AOC-4 (e-form). (Ministry of Corporate Affairs, 2013)

In case, there is no AGM held by the company, then it may file the financial statement with such additional fees within the time prescribed under Section 403 of the Act.

Penalty for not filing MCA annual return

The penalty for a company not filing MCA annual return is INR 5 lakhs. In addition, every officer of the company who is in default will be punishable with imprisonment for a term of up to 6 months or with a fine or both. In addition, companies that do not file their income tax return or MCA annual return continuously can be marked as a strike off by the Registrar of Companies. Before the company is striked off, the bank accounts of the company could also be frozen.

Finally, once a company is marked as strike off by the Registrar of Companies, the directors in the company would be disqualified from acting as Director of a company for a period of 5 years.

To explore business opportunities, link with me by clicking on the 'Invite' button on my eBiz Card.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views, official policy or position of GlobalLinker.

View Shruti 's profile

Other articles written by Shruti Aggarwal

9 modes of funding for your startup

264 week ago

6 tips to grow your startup faster

266 week ago

Annual compliance checklist for startups

288 week ago

Most read this week

Comments

Share this content

Please login or Register to join the discussion